Signs of identity theft: How to recognize warning signs early

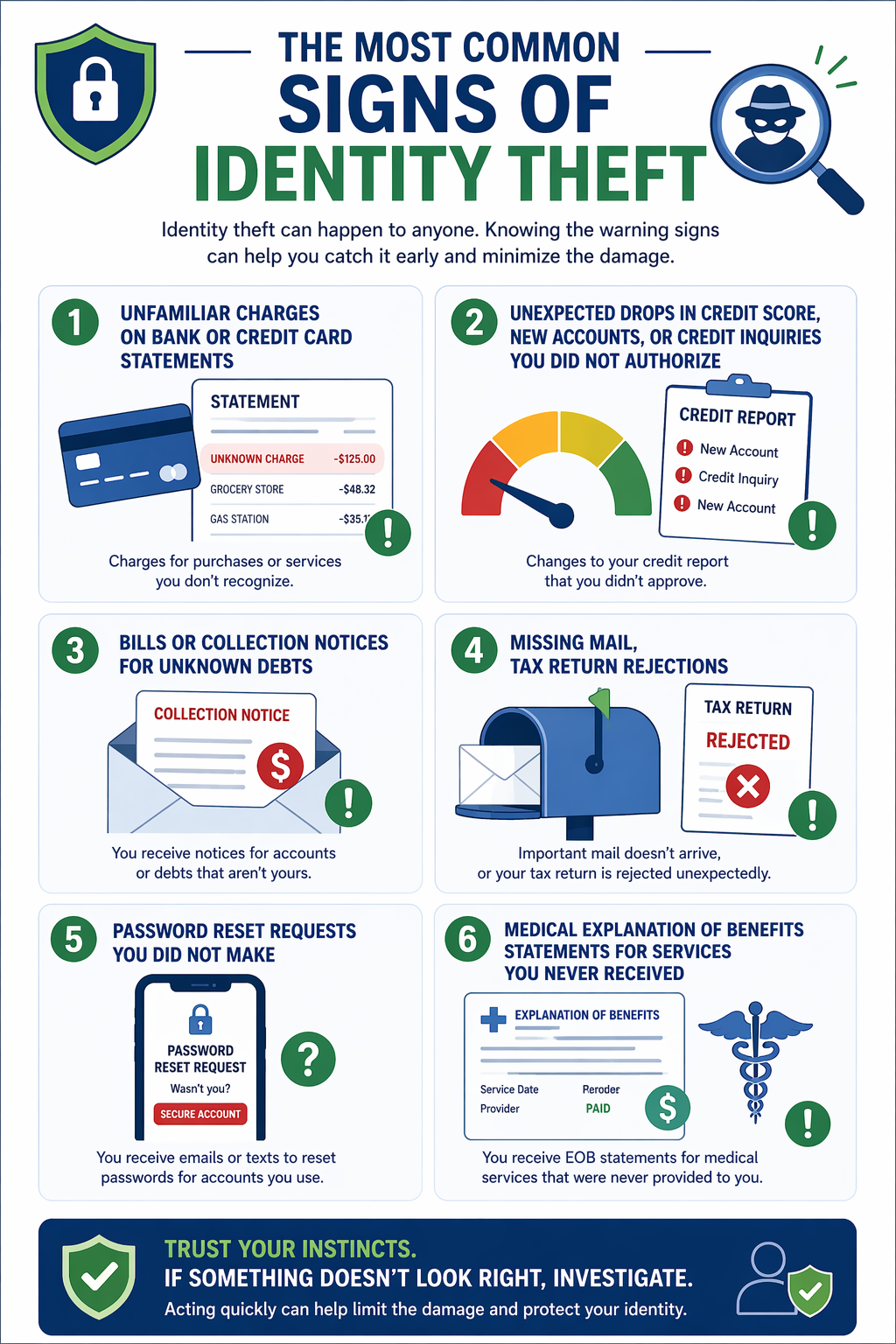

The most common signs of identity theft

- Unfamiliar charges on bank or credit card statements

- Unexpected drops in credit score, new accounts, or credit inquiries you did not authorize

- Bills or collection notices for unknown debts

- Missing mail or tax return rejections

- Password reset requests you did not make

- Medical Explanation of Benefits statements for services you never received

The FBI says the Internet Crime Complaint Center (IC3) now receives nearly 3,000 complaints a day.1 That means thousands of people woke up today to find their identity compromised.

By the time most people notice something is wrong, criminals have already had days, weeks, or months to do damage. The sooner you catch the signs, the better your chances of limiting the fallout.

“The longer ID theft goes on, the more damage is done, and the longer it takes the victim to recover from it,” said Eva Velasquez, President and CEO of the Identity Theft Resource Center, a nationally recognized nonprofit that has assisted identity crime victims since 1999.2

- Identity theft often goes undetected for weeks or months; early recognition is the most effective form of protection

- The most common warning signs span financial accounts, mail, tax records, digital accounts, and medical insurance

- Credit card fraud remains the single most reported type of identity theft

- A sudden credit score drop, unfamiliar accounts, or unauthorized inquiries are strong indicators that someone is using your identity

- Once you spot a warning sign, acting within 24 hours (placing a fraud alert, filing with the FTC, and notifying your bank) significantly limits the damage

- Ongoing monitoring matters even after resolving fraud, because exposure from just one breach can lead to repeat attempts

How to tell if your identity has been stolen

Identity theft often begins without any obvious signal. Criminals may use stolen personal information for weeks or months before a victim notices anything unusual. According to the Federal Trade Commission’s 2024 Consumer Sentinel report, identity theft reports increased 9.5% year over year, reaching 1,135,270 complaints.3 Total fraud losses hit $12.5 billion, a 25% jump from the prior year. These numbers likely don’t capture the full picture, because many victims never report incidents and many cases go undetected for months.

The Javelin Strategy & Research 2024 Identity Fraud Study found that consumers spent an average of 10 hours resolving fraud in 2023, up from six hours the year before.4 60% of victims required several weeks to regain control of their identity. The earlier you catch the signs, the better your chances of reducing the time, cost, and stress that follow.

This guide from OmniWatch breaks down the most common warning signs of identity theft, from financial red flags to online account issues, and explains what to do if you spot them.

Common signs of identity theft at a glance

Financial signs of identity theft

Financial accounts are the most common place where signs of identity theft first become visible. These warning signs typically appear on bank statements, credit card bills, and credit reports.

Unfamiliar charges on bank or credit card statements

Small, unfamiliar charges on a checking account or credit card are one of the earliest signs of identity theft.

Criminals frequently test stolen card information with minor purchases, sometimes as low as $1 or $2, before attempting larger transactions. Credit card fraud remained the most reported type of identity theft in 2025, with over 540,000 cases reported through the first three quarters of the year, according to FTC Consumer Sentinel data.5 If you spot a charge you do not recognize, contact your financial institution immediately to dispute it and request a replacement card.

Unexpected credit score changes

A sudden drop in your credit score without an obvious explanation can be a sign that someone opened accounts or took on debt in your name.

The Experian 2025 U.S. Identity and Fraud Report found that identity theft (68%) and stolen credit card data (61%) topped the list of consumer concerns for the second year in a row.6 Federal law entitles every consumer to one free credit report per year from each of the three major bureaus through AnnualCreditReport.com.7 Reviewing your report at least quarterly can help you catch unauthorized activity before it snowballs.

Accounts or credit inquiries you did not authorize

Hard credit inquiries that you did not initiate are a strong sign that someone is attempting to open accounts using your personal information.

New credit cards, store accounts, or loans appearing on your credit report confirm identity theft has already occurred. According to Security.org’s analysis of FTC data, identity theft complaints reached 1,135,270 in 2024, a 9.5% increase from the prior year.8 If you notice unfamiliar inquiries, place a fraud alert or credit freeze with all three major credit bureaus (Equifax, Experian, and TransUnion) immediately.

Bills or collection notices for accounts you never opened

Receiving bills or collection notices for debts you have no knowledge of is a serious sign of identity theft.

These documents may arrive by mail or email and reference accounts at retailers, medical providers, or financial institutions you have never used. Do not ignore collection notices. Contact the creditor to dispute the account and file a report at IdentityTheft.gov, which can help you create a personalized recovery plan.9

Mail and communication signs of identity theft

Changes to mail delivery and unexpected communications from unfamiliar institutions can be easy to dismiss, but they are often early signs of identity theft that indicate a criminal is intercepting your information or opening new accounts in your name.

Missing mail or redirected financial statements

If bank statements, credit card bills, or other financial documents stop arriving, it may mean someone has submitted a change-of-address request in your name to redirect your mail.

Criminals use this tactic to delay detection while they open and use fraudulent accounts. Contact the U.S. Postal Service to verify your address on file and reach out to each financial institution if expected statements have not arrived.

Unexpected correspondence from unfamiliar companies

Welcome letters, account confirmations, or promotional materials from companies you have never done business with can signal that someone used your information to create new accounts.

Pay close attention to any correspondence from insurance companies, utilities, or financial institutions you do not recognize. These communications are often the first tangible evidence of identity misuse.

Calls from debt collectors about debts you do not owe

Calls from collection agencies about debts you never incurred are a serious sign of identity theft.

Ask for written verification of the debt before providing any personal information. Under the Fair Debt Collection Practices Act, you are entitled to a validation notice within five days of the initial contact. If the debt is fraudulent, file a dispute with the credit bureaus and report the theft to the FTC.

Tax and government-related signs of identity theft

Government records and tax filings are high-value targets because they provide access to refunds and benefits. Tax-related identity theft can also take significantly longer to resolve than other forms.

Tax return rejected as a duplicate filing

Learning that your tax return has been rejected because a return was already filed using your Social Security number is one of the most serious signs of identity theft.

The IRS Taxpayer Advocate Service reported that identity theft victim assistance cases averaged 506 days to resolve in fiscal year 2025, down from 676 days the prior year.10 If your return is rejected as a duplicate, file IRS Form 14039 (Identity Theft Affidavit) and consider enrolling in the IRS Identity Protection PIN program.

Unfamiliar government benefit claims in your name

Receiving a notice about benefits you never applied for, such as unemployment insurance, Social Security, or Medicare claims, is a sign of identity theft.

Employment-related identity theft totaled 37,556 reported cases in 2024, a 20% year-over-year increase according to Security.org.8 Report suspicious benefit claims directly to the issuing agency.

Digital and online signs of identity theft

Online identity fraud now represents more than 70% of all identity fraud activity, according to industry research.11 Digital warning signs have become some of the most important indicators that your personal information has been compromised.

Password reset notifications you did not request

If you receive password reset emails or two-factor authentication codes you did not request, someone may be trying to access your accounts.

Change the password on any affected account immediately, enable two-factor authentication if it is not already active, and review account activity for unauthorized logins. This is especially urgent when the notifications come from financial institutions or email providers.

Unfamiliar login activity or account lockouts

Login activity from unfamiliar devices or locations, or being locked out of your own account without explanation, are signs of identity theft in the digital space.

The Identity Theft Resource Center’s 2025 Consumer Impact Report found that social media takeover was the most commonly reported form of identity misuse in 2025, affecting 35.3% of general consumer victims.12 That figure was up from 29.4% the prior year, reflecting a growing trend toward account-based identity crimes.

Data breach notifications

A data breach notification means your personal information is circulating beyond your control.

The Identity Theft Resource Center’s 2025 Data Breach Report found that 88% of people who received a breach notice experienced at least one negative consequence, including targeted phishing attempts (54%) and attempted account takeovers (40%).13 Change affected passwords, monitor your credit, and consider using a dark web monitoring service to track whether your exposed data surfaces on underground marketplaces.

Medical and insurance signs of identity theft

Medical identity theft can be particularly dangerous because it affects both your finances and your health records. In some cases, a thief’s medical history can become merged with yours, potentially leading to incorrect diagnoses or wrong prescriptions.

Explanation of Benefits for services you did not receive

If a health insurance Explanation of Benefits (EOB) statement lists medical services, prescriptions, or procedures you never received, someone may be using your health insurance information.

Medical identity theft accounted for 10,116 reports in recent FTC data, according to Security.org.8 Review every EOB statement carefully, even when you have not visited a provider recently.

Health insurance claims are denied due to reaching benefit limits

If a legitimate health insurance claim is denied because records show you already reached your benefit ceiling, it can indicate that someone else used your insurance.

Request a full claims history from your insurer and report any discrepancies immediately. Medical identity theft is among the most difficult types to detect and resolve because it involves both financial and healthcare systems.

Less obvious signs of identity theft that people often miss

Sudden increase in phishing emails, spam, or robocalls

A sharp spike in spam messages, phishing emails, or robocalls can mean your personal information was exposed in a data breach or sold on the dark web.

The ITRC’s 2025 Data Breach Report found that 49% of breach victims experienced an increase in spam emails or robocalls after their information was compromised.12 While spam alone is not identity theft, it frequently precedes more targeted fraud attempts. Tools that detect suspicious messages early can help you avoid taking the next step a scammer is hoping for.

Unfamiliar addresses appearing on your credit report

Credit reports include a history of addresses associated with your name.

If an address you have never lived at appears on your report, it could mean someone is using your name and Social Security number at that location. Request corrections from the credit bureau and investigate the source of the unfamiliar address.

Unexplained difficulty obtaining credit

If you are unexpectedly denied credit, offered unfavorable terms, or quoted higher interest rates without a clear reason, identity theft may be affecting your credit profile.

If your financial history does not explain the denial, review your credit reports carefully for unauthorized accounts, late payments, or collection items that do not belong to you. Personal data is constantly being stored, shared, and exposed across online transactions, creating potential exposure points that identity thieves can exploit.

What to do if you spot signs of identity theft

If you notice any of these warning signs, acting quickly is essential. The Javelin 2024 Identity Fraud Study found that 60% of identity theft victims needed several weeks to regain control.4 These steps can help reduce that timeline:

- Place a fraud alert or credit freeze. Contact one of the three major credit bureaus to place a fraud alert, which requires creditors to verify your identity before opening new accounts. For stronger protection, request a credit freeze at each bureau. OmniWatch offers a one-click credit freeze feature that simplifies this process.

- File a report at IdentityTheft.gov. The FTC’s portal creates a personalized recovery plan and generates pre-filled dispute letters and an official identity theft report.

- File a police report. A police report may be required documentation when disputing fraudulent accounts with creditors and financial institutions.

- Notify affected financial institutions. Contact your bank, credit card issuers, and any financial institution where fraudulent activity occurred. Request that fraudulent accounts be closed and charges reversed. Ask for written confirmation of the resolution.

- Change passwords and enable two-factor authentication. Update passwords on compromised accounts and any accounts sharing the same credentials. Use unique, complex passwords for each account.

- Monitor your credit and personal information continuously. Even after addressing immediate fraud, ongoing monitoring is critical. An identity protection service like OmniWatch that provides credit monitoring, dark web surveillance, and real-time alerts can detect new instances of misuse before they cause additional damage.

Why early detection of identity theft signs matter

Identity theft does not announce itself. It shows up as a charge you almost scroll past, a piece of mail that never arrives, or a tax return that gets rejected without explanation. By the time many victims realize what has happened, the damage is already compounding. The signs covered in this guide are not rare edge cases—they are the everyday signals that fraud is underway.

The good news is that awareness works. Reviewing your financial statements regularly, checking your credit report quarterly, and using a monitoring service that watches for threats around the clock puts you in a position to catch fraud early (when it is still manageable). The difference between catching identity theft in week one versus month six can mean hundreds of hours of recovery time and thousands of dollars in losses.

Protecting your identity is not a one-time action. It is an ongoing habit, and it starts with knowing what to look for.

Most identity theft victims only discover fraud after the damage is done. OmniWatch monitors your credit, the dark web, and your inbox in real time so you catch threats before they become crises.

With OmniWatch Elite, you get:

- Real-time credit monitoring across all three bureaus

- Dark web surveillance for your personal information

- AI-powered Auto-scan scam detection in your Gmail and Outlook

- One-click credit freeze capability

- 24/7 identity restoration specialists

- Up to $4 million in identity theft insurance

Already seeing warning signs? Our restoration agents are ready to help you take action now.

Frequently asked questions about signs of identity theft

What is the most common sign of identity theft?

The most common sign of identity theft is unfamiliar charges on your bank or credit card statements. Criminals often test stolen card data with small purchases before attempting larger transactions. Credit card fraud was the single most reported type of identity theft in the United States in 2024, based on FTC Consumer Sentinel data.

How quickly should I act if I notice signs of identity theft?

Immediately. Place a fraud alert or credit freeze, report the suspected theft at IdentityTheft.gov, and notify affected financial institutions within 24 hours. The faster you respond, the better your chances of limiting the damage. The Javelin 2024 study found that consumers spent an average of 10 hours resolving identity fraud, and that timeline increases the longer fraud goes undetected.4

Can identity theft happen even if I am careful with my personal information?

Yes. Data breaches at corporations, healthcare providers, and government agencies can expose personal information regardless of individual security practices. The ITRC’s 2025 Data Breach Report found that 88% of breach notification recipients experienced at least one negative consequence, including targeted phishing attempts and account takeover attempts.13

What is the difference between a fraud alert and a credit freeze?

A fraud alert asks creditors to verify your identity before opening new accounts. It lasts one year and can be renewed. A credit freeze blocks all new access to your credit file until you choose to lift it. A freeze provides stronger protection and is recommended if you have confirmed that your identity has been compromised.

How does OmniWatch help detect signs of identity theft?

OmniWatch Elite provides real-time credit monitoring, dark web surveillance, data breach alerts, and AI-powered scam detection that can surface warning signs of identity theft early. Members also have access to 24/7 identity restoration agents and up to $4 million in identity theft insurance if fraud occurs. The platform monitors credit file changes, dark web exposure, and incoming emails for phishing threats, giving members a comprehensive view of their identity security.

What are the signs of identity theft on a credit report?

Common signs of identity theft on a credit report include unfamiliar accounts, hard inquiries you did not authorize, addresses where you have never lived, and collection items for debts you do not recognize. Reviewing your credit report at least quarterly through AnnualCreditReport.com is one of the most reliable ways to spot identity theft early.7

This guide is published by OmniWatch. Follow OmniWatch on Facebook for ongoing guidance on identity protection, digital safety, and scam awareness.

1 FBI, Internet Crime Report 2025, 2025

2 Identity Theft Resource Center, ITRC Homepage, 2025

3 Federal Trade Commission, Consumer Sentinel Network Data Book 2024, 2025

4 Javelin Strategy & Research, 2024 Identity Fraud Study, 2024

5 Federal Trade Commission, Consumer Sentinel Data 2025, 2025

6 Experian, 2025 U.S. Identity and Fraud Report, 2025

7 AnnualCreditReport.com, Free Credit Reports

8 Security.org, Identity Theft Statistics, 2025

9 Federal Trade Commission, IdentityTheft.gov

10 IRS Taxpayer Advocate Service, Identity Theft Awareness and Update on IRS Processing, 2025

11 Snappt, Identity Fraud Statistics, 2025

12 Identity Theft Resource Center, 2025 Consumer Impact Report, 2025

13 Identity Theft Resource Center, 2025 Annual Data Breach Report, 2025